July 2026 continued the broader trend of moderating electricity prices across the National Electricity Market, though the pace of decline slowed relative to recent months. Key developments during the month included:

- NEM spot prices fell 29.3% year-on-year to $76.85/MWh, with Queensland again the lowest-priced mainland state at $65.43/MWh

- South Australia remained the highest-priced mainland state at $95.89/MWh, as a significant reduction in wind output drove heavier reliance on gas generation and imports

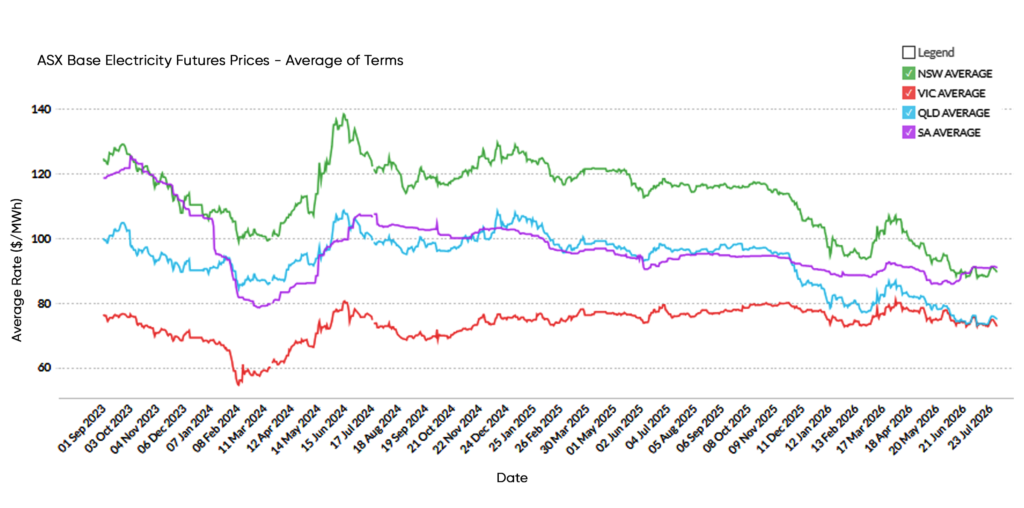

- Forward electricity prices were largely stable across all regions, with New South Wales and Queensland continuing to trade at multi-year lows well below their 3-year averages

- Renewable generation rose to 39.9% of total supply — just short of the 40% threshold — supported by strong growth in solar and hydro output, even as wind generation declined

- Battery discharge continued its rapid acceleration, rising 184% year-on-year to a record 492 GWh

These outcomes point to a market settling into a more consolidated phase after an extended period of repricing. While the national trend remained favourable, South Australia’s experience illustrates how quickly regional conditions can shift when wind resource underperforms.

National Electricity Update

Spot Prices

Spot prices across the National Electricity Market (NEM) declined year-on-year in July 2026, with all regions recording lower average prices than July 2025. July 2025 was an elevated month across the NEM — particularly in SA ($164.95/MWh) and TAS ($117.85/MWh) — making the year-on-year comparisons appear large in those states.

The NEM average fell 29.3% to $76.85/MWh. NSW and VIC recorded the most modest declines at -15.9% and -14.3% respectively, while SA (-41.8%) and TAS (-39.7%) fell most sharply in percentage terms against their elevated prior-year bases. QLD at $65.43/MWh was again the lowest-priced mainland state. SA at $95.89/MWh remained the highest, underpinned by a significant drop in wind output and heavier reliance on gas and imports during the month.

| Region | Jul-25 ($/MWh) | Jul-26 ($/MWh) | % Movement |

|---|---|---|---|

| NSW | 96.95 | 81.52 | -15.9% |

| QLD | 82.13 | 65.43 | -20.3% |

| SA | 164.95 | 95.89 | -41.8% |

| TAS | 117.85 | 71.04 | -39.7% |

| VIC | 82.13 | 70.36 | -14.3% |

| NEM Avg | 108.80 | 76.85 | -29.3% |

Futures Prices

July was a notably quiet month for forward market movement. All regions moved by less than 4% on the average of terms, reflecting a market in consolidation following several months of sustained repricing. The forward curve structure remains broadly unchanged — NSW and QLD are sitting at multi-year lows well below their 3-year averages, SA is tracking modestly below its benchmark despite its spot spike, and VIC continues to trade near par with its long-term average.

NSW at $89.71/MWh and QLD at $75.21/MWh have both been at these levels only briefly since early 2022, reinforcing the scale of the repricing that has occurred over the past 18 months. VIC at $73.02/MWh is effectively at its 3-year average (-1.0%), the only region where forward prices still reflect structural supply tightness as brown coal capacity retires.

| Region | Month Open | Month Close | % Movement | 3yr Avg | vs 3yr Avg |

| NSW | 90.63 | 89.71 | -1.0% | 113.33 | -20.8% |

| QLD | 75.88 | 75.21 | -0.9% | 93.35 | -19.4% |

| SA | 90.85 | 91.12 | +0.3% | 98.02 | -7.0% |

| VIC | 75.44 | 73.02 | -3.2% | 73.79 | -1.0% |

| NEM (Avg) | 83.20 | 82.27 | -1.1% | 94.62 | -13.1% |

Generation Mix

Total NEM generation rose modestly year-on-year (+1.0%) to 19,970 GWh, the highest July output on record according to OpenNEM data. The renewable share lifted to 39.9%, just short of 40%, driven primarily by strong solar growth (+19.9%) and a significant increase in hydro output (+33.2%). Wind generation fell 11.6% — a meaningful decline — partially offsetting the gains from solar and hydro.

Battery discharge continued its rapid acceleration, rising 184% year-on-year to 492 GWh — the highest monthly figure recorded to date. Gas generation fell 22.7%, with coal broadly flat (-0.9%). Emissions intensity improved modestly to 566 kgCO₂e/MWh (-2.2%).

| Metric | Jul-25 | Jul-26 | Change |

|---|---|---|---|

| Total generation (GWh) | 19,769 | 19,970 | +1.0% |

| Renewable share (%) | 38.3% | 39.9% | +1.6 % |

| Coal share (%) | 56.3% | 55.2% | -1.1 % |

| Gas share (%) | 5.6% | 4.3% | -1.3 % |

| Wind (GWh) | 3,746 | 3,311 | -11.6% |

| Solar (GWh) | 2,769 | 3,320 | +19.9% |

| Hydro (GWh) | 1,157 | 1,541 | +33.2% |

| Battery discharge (GWh) | 173 | 492 | +184% |

| Emissions intensity (kgCO₂e/MWh) | 579 | 566 | -2.2% |

State Electricity Update

New South Wales

Spot

NSW average spot prices fell to $81.52/MWh from $96.95/MWh in July 2025 (-15.9%). This was the most modest year-on-year decline on the mainland, reflecting that NSW did not experience the same degree of price spike in July 2025 as SA or TAS. The July 2026 outcome is broadly consistent with the recent trend, sitting below the state’s 12-month average and in line with the softer pricing environment that has characterised the NEM since late 2025.

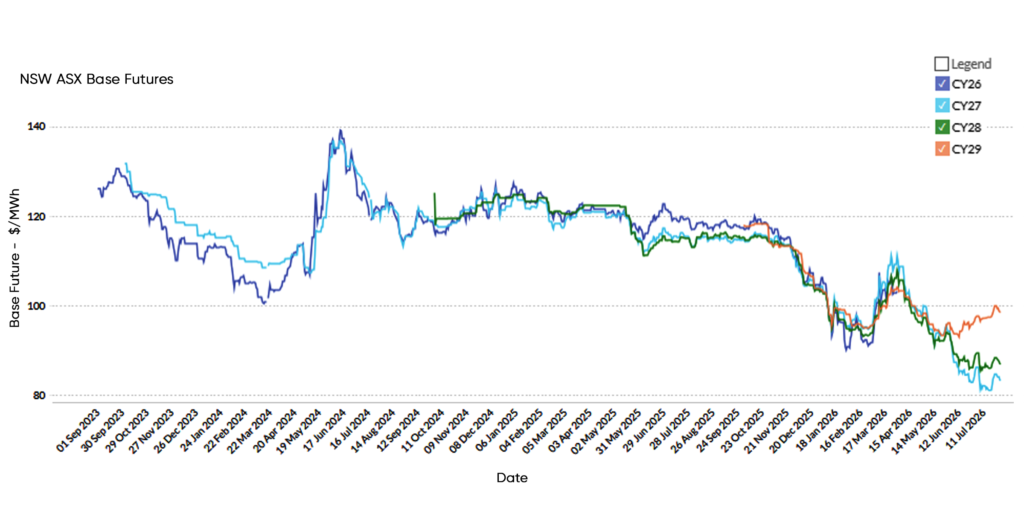

Futures

| Contract | Month Open | Month Close | % Change |

|---|---|---|---|

| CY27 | 85.63 | 83.43 | -2.6% |

| CY28 | 89.02 | 87.05 | -2.2% |

| CY29 | 97.25 | 98.65 | +1.4% |

NSW forward prices eased slightly across CY27 (-2.6%) and CY28 (-2.2%), with CY29 edging marginally higher (+1.4%). The pattern reflects a broadly stable market with a slight flattening of the forward curve. The average of terms closed at $89.71/MWh — essentially unchanged from June — and remains 20.8% below the 3-year average, its lowest level since February 2022. The persistent gap to the long-term benchmark continues to present a compelling case for longer-term contract fixation.

Generation Mix

| Metric | Jul-25 | Jul-26 | Change |

|---|---|---|---|

| Total generation (GWh) | 7,257 | 7,124 | -1.8% |

| Renewable share (%) | 28.3% | 30.3% | +2.0% |

| Coal (GWh) | 4,470 | 4,176 | -6.6% |

| Gas (GWh) | 195 | 57 | -70.8% |

| Wind (GWh) | 858 | 693 | -19.2% |

| Solar (GWh) | 1,028 | 1,282 | +24.7% |

| Hydro (GWh) | 180 | 226 | +25.6% |

| Battery discharge (GWh) | 30 | 176 | +487% |

| Imports (GWh) | 695 | 779 | +12.1% |

| Emissions intensity (kgCO₂e/MWh) | 620 | 590 | -4.8% |

NSW total generation declined 6.5% to 6,529 GWh. Renewable share improved by 2.8 percentage points to 29.0%, supported by stronger wind (+14.4%) and hydro (+8.1%) output. Coal generation fell 11.5% and gas declined 31.4%, the latter continuing a multi-month downward trend. Battery discharge increased significantly from 24.9 GWh to 95 GWh (+281%), reflecting the rapid expansion of storage capacity in the state. Emissions intensity improved 6.6% to 593 kgCO₂e/MWh.

Queensland

Spot

QLD average spot prices fell to $65.43/MWh from $82.13/MWh (-20.3%), the lowest monthly average of any mainland state in July. The result continues the pattern of QLD pricing well below other regions, supported by strong renewable penetration and relatively contained demand growth. At $65.43/MWh, QLD sits materially below its 12-month average, consistent with the ongoing softening in NEM-wide pricing conditions.

Futures

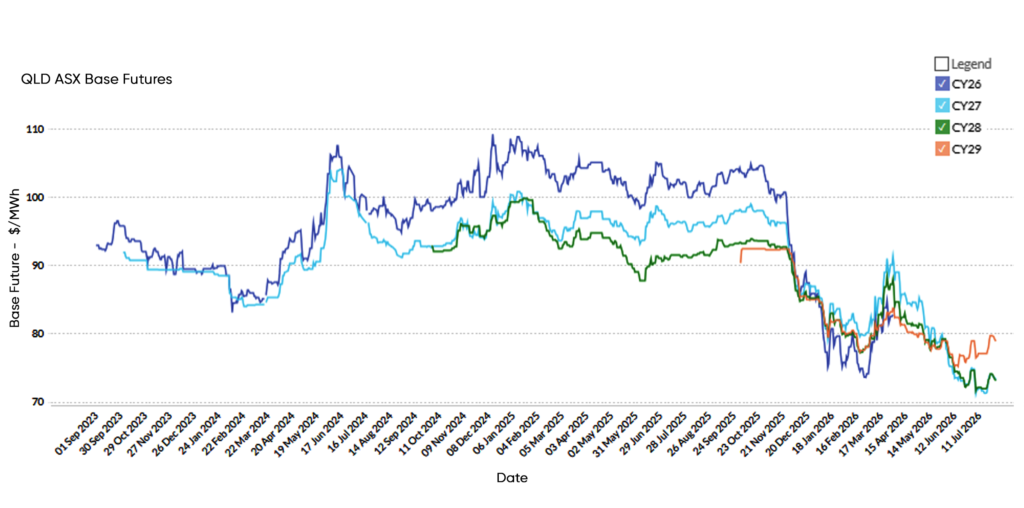

| Contract | Month Open | Month Close | % Change |

|---|---|---|---|

| CY27 | 74.77 | 73.32 | -1.9% |

| CY28 | 74.52 | 73.27 | -1.7% |

| CY29 | 78.35 | 79.04 | +0.9% |

QLD forward prices were essentially flat across CY27 (-1.9%) and CY28 (-1.7%), with CY29 edging fractionally higher (+0.9%). The curve remains remarkably flat at around $73-$79/MWh across all contracts, signalling that the market sees limited escalation risk over the medium term. At $75.21/MWh on the average of terms, QLD is 19.4% below its 3-year average — the second-deepest discount of any mainland state after NSW.

Generation Mix

| Metric | Jul-25 | Jul-26 | Change |

|---|---|---|---|

| Total generation (GWh) | 5,285 | 5,302 | +0.3% |

| Renewable share (%) | 32.2% | 38.0% | +5.8% |

| Coal (GWh) | 3,645 | 3,896 | +6.9% |

| Gas (GWh) | 353 | 196 | -44.5% |

| Wind (GWh) | 465 | 535 | +15.1% |

| Solar (GWh) | 1,118 | 1,316 | +17.7% |

| Battery discharge (GWh) | 50 | 165 | +230% |

| Imports (GWh) | 31 | 5 | -83.9% |

| Emissions intensity (kgCO₂e/MWh) | 606 | 580 | -4.3% |

QLD generation was broadly flat at 5,302 GWh (+0.3%). Renewable share rose 5.8 percentage points to 38.0%, driven by strong growth in both solar (+17.7%) and wind (+15.1%). Coal generation rose 6.9% — an increase that appears to reflect higher total system demand rather than renewable displacement — while gas fell sharply (-44.5%). Battery discharge grew 230% from 50 to 165 GWh, continuing the accelerating trend across the NEM. Emissions intensity improved 4.3% to 580 kgCO₂e/MWh.

Victoria

Spot

VIC average spot prices fell to $70.36/MWh from $82.13/MWh (-14.3%), the second-most modest year-on-year decline on the mainland after NSW. VIC’s July 2025 reference price was not elevated to the same degree as SA or TAS, making the year-on-year comparison more representative of underlying market conditions. The July 2026 outcome is consistent with the recent trend of VIC pricing as the second-lowest mainland state after QLD.

Futures

| Contract | Month Open | Month Close | % Change |

|---|---|---|---|

| CY27 | 65.52 | 62.02 | -5.3% |

| CY28 | 76.44 | 72.26 | -5.5% |

| CY29 | 84.35 | 84.77 | +0.5% |

VIC was the most active state in the forward market during July, with CY27 falling 5.3% and CY28 declining 5.5% — the largest moves of any state across both contracts. CY29 was essentially flat (+0.5%). The sharp CY27-CY28 reduction brings VIC’s near-term contracts to their lowest levels in some time, though the average of terms at $73.02/MWh remains near its 3-year average (-1.0%). The steepening of the curve — with CY29 at $84.77/MWh well above CY27’s $62.02/MWh — continues to reflect the market’s expectation of tighter supply conditions in the outer years as brown coal retires.

Generation Mix

| Metric | Jul-25 | Jul-26 | Change |

|---|---|---|---|

| Total generation (GWh) | 4,866 | 5,213 | +7.1% |

| Renewable share (%) | 41.6% | 40.6% | -1.0 % |

| Coal (GWh) | 3,024 | 3,165 | +4.7% |

| Gas (GWh) | 144 | 123 | -14.6% |

| Wind (GWh) | 1,516 | 1,332 | -12.1% |

| Solar (GWh) | 394 | 477 | +21.1% |

| Hydro (GWh) | 143 | 359 | +151% |

| Battery discharge (GWh) | 53 | 112 | +111% |

| Imports (GWh) | 165 | 295 | +78.8% |

| Emissions intensity (kgCO₂e/MWh) | 695 | 691 | -0.6% |

VIC total generation rose 7.1% to 5,213 GWh — the largest increase of any state and the highest July total on record for Victoria. The increase was driven by strong hydro output, which more than doubled year-on-year from 143 to 359 GWh (+151%), and solar growth (+21.1%). Wind fell 12.1%, consistent with the NEM-wide trend of lower wind resource in July 2026. Battery discharge doubled to 112 GWh. Coal generation rose 4.7%, while gas fell 14.6%. Renewable share edged slightly lower (-1.0 pp) to 40.6%, as the coal and hydro increases outweighed the decline in wind. Emissions intensity was broadly flat at 691 kgCO₂e/MWh (-0.6%).

South Australia

Spot

SA average spot prices fell to $95.89/MWh from $164.95/MWh (-41.8%). Despite the large year-on-year decline, SA was again the highest-priced mainland state in July 2026. This outcome is directly linked to a significant reduction in wind generation during the month — wind output fell 25% year-on-year to 559 GWh — which forced greater reliance on gas and a near-doubling of imports from Victoria. The combination of lower renewable output and tighter dispatchable supply drove SA’s spot average above $95/MWh while other mainland states settled below $82/MWh.

Futures

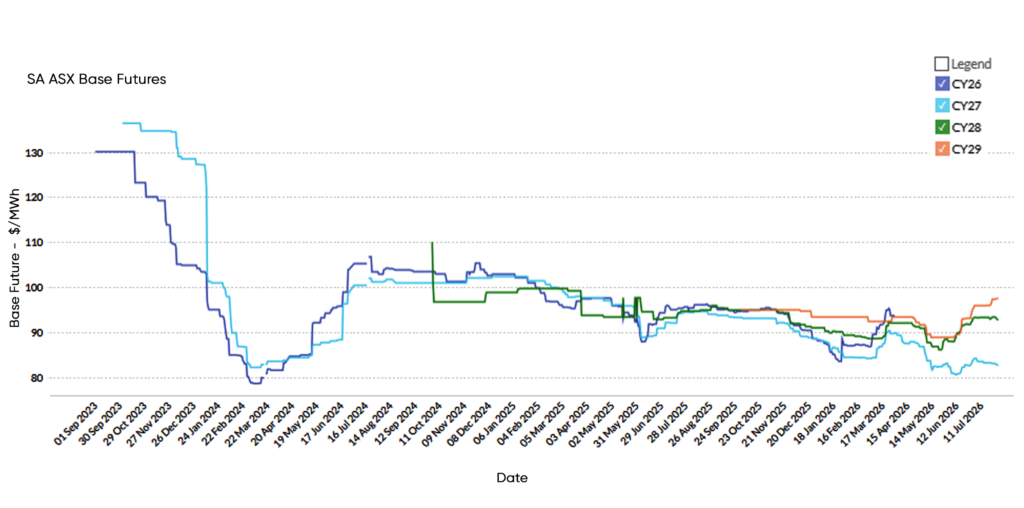

| Contract | Month Open | Month Close | % Change |

|---|---|---|---|

| CY27 | 84.05 | 82.83 | -1.5% |

| CY28 | 93.15 | 92.91 | -0.3% |

| CY29 | 95.34 | 97.61 | +2.4% |

SA forward prices were broadly stable in July, with CY27 easing slightly (-1.5%), CY28 essentially flat (-0.3%), and CY29 rising 2.4%. The shape of the SA curve — with outer years pricing above near-term contracts — reflects ongoing market concern about SA’s supply adequacy as the state’s renewable share grows and gas firming capacity remains limited. SA sits 7.0% below its 3-year average on the average of terms, a smaller discount than NSW or QLD.

Generation Mix

| Metric | Jul-25 | Jul-26 | Change |

|---|---|---|---|

| Total generation (GWh) | 61,388 | 1,350 | -2.7% |

| Renewable share (%) | 66.6% | 55.9% | -10.7 % |

| Gas (GWh) | 394 | 406 | +3.0% |

| Wind (GWh) | 745 | 559 | -25.0% |

| Solar (GWh) | 211 | 224 | +6.2% |

| Battery discharge (GWh) | 40 | 39 | -2.5% |

| Imports (GWh) | 110 | 210 | +90.9% |

| Emissions intensity (kgCO₂e/MWh) | 203 | 264 | +28.2% |

SA total generation fell 2.7% to 1,350 GWh. The headline story is a 10.7 percentage point decline in renewable share to 55.9%, driven almost entirely by the sharp drop in wind output (-25.0%). Solar generation grew modestly (+6.2%), but was insufficient to offset the wind shortfall. Gas generation rose 3.0% and imports surged 90.9% to 210 GWh as the state drew heavily on interconnector flows to fill the gap. Emissions intensity rose significantly to 264 kgCO₂e/MWh (+28.2%), the largest year-on-year deterioration of any state.

Closing Commentary

July reflected a period of consolidation across the National Electricity Market, following several months of more pronounced repricing. Forward prices held broadly steady across all regions, with New South Wales and Queensland maintaining their positions at multi-year lows relative to long-term averages — suggesting the market has settled into a new, lower pricing range rather than continuing to reprice further downward in the near term.

South Australia’s outcome during July serves as a useful reminder that the transition toward a higher-renewable system does not remove supply-side variability; it changes its nature. A 25% year-on-year fall in wind output was sufficient to push the state’s spot prices above all other mainland regions, despite a substantial year-on-year decline compared to July 2025.

Record levels of battery discharge and continued growth in solar and hydro output underline the pace at which storage and renewable capacity are being deployed across the NEM. As this build-out continues, the interaction between variable generation, storage dispatch and regional supply conditions will remain central to understanding short-term price movements. Leading Edge Energy will continue to monitor these developments closely to help clients navigate changing market conditions, manage risk and make informed energy procurement decisions.

Explainer: Why we focus on Wholesale Futures Prices

Wholesale Futures Price: This reflects what the market expects wholesale electricity spot rates to be in future periods. The offers that commercial and industrial (C&I) customers receive via Leading Edge Energy are closely correlated to wholesale prices on the ASX Energy futures market; this is why we focus on these prices in our commentary.

Spot Price: This represents how much the spot market is charging for electricity currently based on demand and supply. Spot prices go up when demand is high and supply is tight.

You can learn more about the difference between wholesale electricity futures and spot prices in our blog section.

Disclaimer: The information in this communication is for general information purposes only. It is not intended as financial or investment advice and should not be interpreted or relied upon as such.

We source, analyse, compare and rank commercial, industrial and multi-site energy quotes. Obligation Free.

Chat with one of our experienced consultants today and get the insights your business needs to help manage the risks associated with volatile electricity and natural gas markets. Our energy procurement service is obligation-free and provides a time-saving way of securing lower energy rates from our panel of energy retailers.

Get advice from our Energy Management Consultants

Ewen Beard

Sales Manager

Get in Touch

Feel free to call or e-mail us. Or just fill in the form below and we’ll contact you for an obligation-free discussion.

Are you ready to save on business energy costs?

Get StartedLeading Edge Energy is proud to be a signatory of the National Customer Code for Energy Brokers, Consultants and Retailers.